"You have power over your mind — not outside events. Realize this, and you will find strength." — Marcus Aurelius, Meditations

Last year I wrote about “the noise” — the constant drumbeat of headlines that tempts investors to abandon their plans. At that time, the noise was about tariffs. Now it's about Iran, the Strait of Hormuz, and oil prices.

You know the basics. U.S. and Israeli strikes against Iranian military targets. Iranian retaliation in the Gulf. The Strait of Hormuz effectively closed. Oil prices jumped. Markets got jittery. The noise got louder.

It's a serious situation. The noise is telling you to panic, but the data is telling you something different.

This isn't your father's oil shock

When most people hear "oil shock," they think 1970s — gas lines, stagflation, recession. That mental model made sense when we were writing checks to OPEC. But the world has changed.

The United States is now a net oil exporter. Dr. David Kelly, Chief Global Strategist at JP Morgan, laid it out plainly: in 2008, the U.S. was spending about 3% of GDP just buying net imports of petroleum. All of that money was leaving the country. Today, we actually export more petroleum than we import. We've gone from writing big checks to OPEC to running a trade surplus in oil.

So when oil prices rise, American oil producers make more money than American consumers lose at the pump. You still get an inflation bump — gas prices sting — but the growth impact is close to a wash. Bottom line: higher oil prices are inflationary for the U.S., but not recessionary. That's a very different story than the 1970s.

Compare this to the 1991 Gulf War, when oil roughly doubled in a matter of weeks. Back then, every component of real GDP fell. But today, Americans spend a much smaller slice of their paychecks on energy than they did back then. The economy's backbone is much healthier now.

Growth forecasts have softened slightly, but the U.S. economy is still expected to grow between 2.0% and 2.5% this year, and the roughly $60 billion in larger tax refunds should roughly balance out the extra pain at the gas pump.

Speed bump, not a cliff.

Meanwhile, underneath the noise

While the headlines have been about Iran, the stuff that actually matters over the medium and long term has been about something else: a massive capital spending cycle led by artificial intelligence.

Companies are spending enormous sums building data centers and AI infrastructure. Analysts are forecasting double-digit S&P 500 earnings growth for the third consecutive year. U.S. productivity has risen at a 2.1% annual rate since the end of 2019, up from 1.5% in the prior cycle — and that improvement has been broad-based. Business investment should broaden beyond AI-adjacent sectors in 2026 as tax policy clarity and a lower cost of capital take hold.

The economy Kelly describes as a "healthy tortoise" — 2% real growth, 4% unemployment, inflation trending toward target — is still plodding along just fine.

What history actually looks like

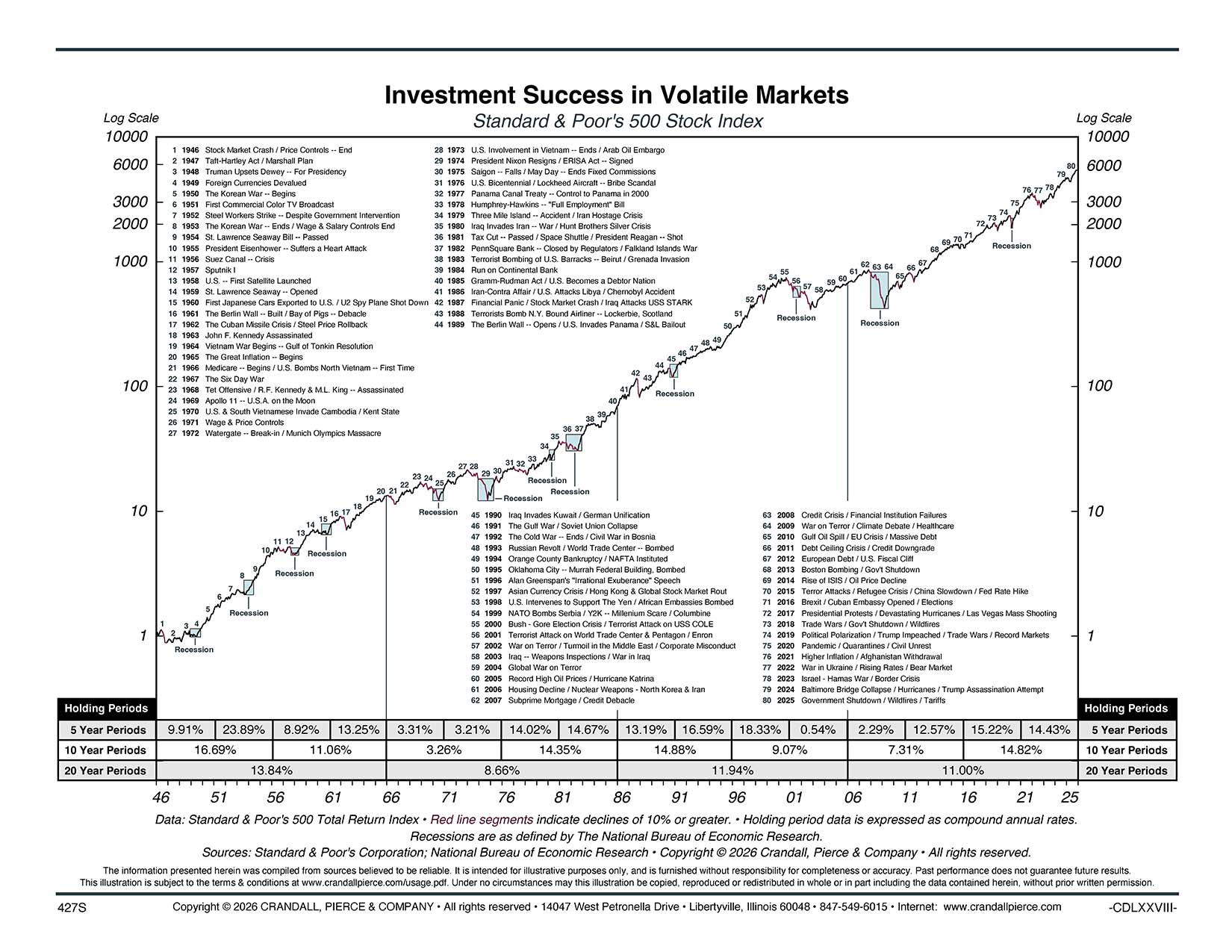

Now I want to show you a chart worth printing out and sticking on your refrigerator.

Click here to download the Investment Success in Volatile Markets chart.

This is a chart of the S&P 500 going back to the late 1940s. Every event that made people want to sell is labeled on it. The Korean War. The Cuban Missile Crisis. Vietnam. Watergate. The oil embargo. Black Monday. The Gulf War. September 11th. The financial crisis. COVID. And now, Iran.

Every one of those felt like the world was ending at the time. And yet, the line goes from the bottom left to the upper right. The red segments show declines of 10% or more. There are a lot of them. They happen regularly. They feel terrible when you're in one. But zoom out, and they're bumps on a very long road.

The data backs it up. Pick any random 5-year period and you made money about 88% of the time. Stretch it to 20 years and you've never lost money — not once, not through wars, pandemics, or financial crises. Looking at annual returns going back to 1928, the market has been positive in about three out of every four years, and the average gain in an up year has been meaningfully larger than the average loss in a down year. The math is overwhelmingly in your favor if you stay in your seat.

The signal and the noise

The situation in Iran will evolve. Oil prices will bounce around. There will be new scary headlines tomorrow and the day after that. That's always been true.

But so has this: the earnings power of the companies you own and compound returns working quietly on your behalf. Let those be your signal. Let the rest be noise.