SUMMARY

This article will explore the ten essential financial literacy topics to help you understand the key aspects of personal finance.

Young Professionals

6 minute read time

This article will explore the ten essential financial literacy topics to help you understand the key aspects of personal finance.

Whether the goal is paying down debt, stashing away cash for something big or just feeling less anxious every time a bill arrives, having a solid financial foundation genuinely changes the game. These topics cover the essentials and mastering them means making smarter decisions, dodging costly mistakes and building the kind of long-term security that actually holds up.

Are you or someone you know starting a new job? Join our campaign to gain essential financial knowledge and explore topics like HSAs, 401ks and investment strategies for a path to financial independence.

ENROLL TODAYFinancial literacy is the ability to understand and effectively manage personal finances. It's about knowing how to budget, save, invest and manage debt — and being clued in on both the risks and the opportunities that come with it. When you build financial literacy, you gain greater control over your financial well-being, make decisions with real confidence and set yourselves up to hit those long-term goals without constantly second-guessing the plan.

Think of financial planning as the GPS for your financial journey — without it, you’re basically just driving around hoping for the best. Starting early is the move, because the earlier you plan, the more runway you have to avoid the stress that comes from being caught off guard. A solid financial plan also takes the edge off major life transitions like buying a home, planning a wedding and preparing for retirement. Connecting with an advisor to get started is always a smart first step.

Budgeting is simply the process of giving every dollar a job. When you know exactly where your money is going, spending feels a lot less stressful and adjustments become intentional rather than reactive. A good starting point? Building out a budget and experimenting with proven techniques like the 50/30/20 method or committing to a no-spend month.

Debt isn't necessarily the villain in the financial story but ignoring it definitely is. Whether it's student loans, credit card balances, auto loans or a mortgage, understanding the terms and repayment options for each type is crucial. Student loans, for example, often come with multiple repayment plans and credit card debt can be chipped away faster by consistently paying more than the minimum. Taking a proactive, strategic approach here leads to real financial stability and a lot less stress.

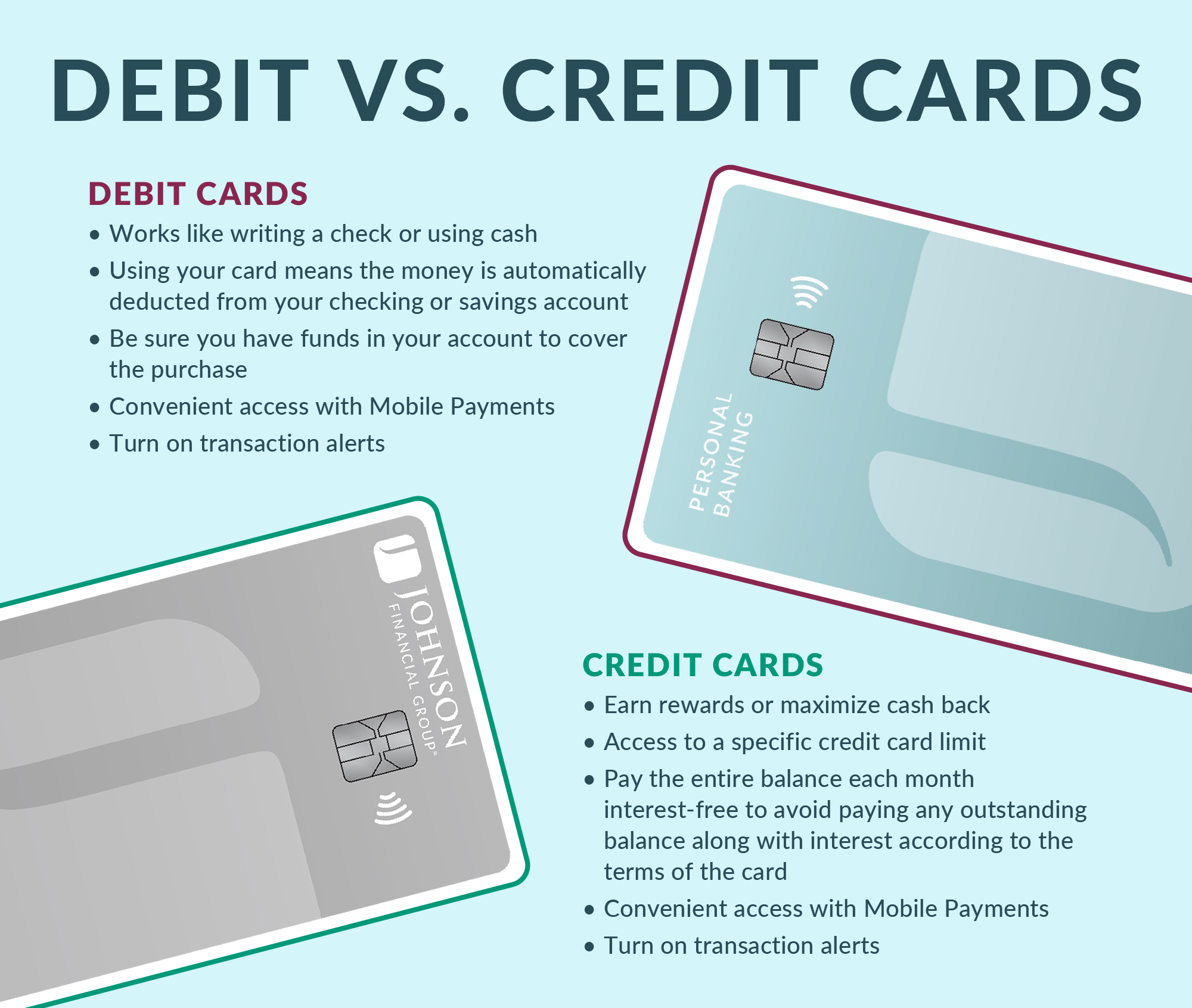

Both credit and debit cards offer convenience but they operate pretty differently. Debit cards keep spending in check by drawing directly from available funds. Credit cards, on the other hand, can actually help build a credit score when used responsibly and many come with solid rewards programs. The key in mastering the credit card? Understanding interest rates, taking advantage of rewards and committing to paying off the balance every single month. When used right, credit cards are a powerful tool.

Your credit score is essentially a financial report card and it plays a huge role in your financial life. It factors in payment history, credit utilization, length of credit history, types of accounts and recent inquiries, all working together to tell lenders how financially trustworthy we are. The good news? Checking your score is free online and there are clear, actionable steps to build and maintain a strong one. Knowing where things stand is the first move.

Big purchasing decisions, like buying a car and deciding whether to rent or own a home, don't come with a universal right answer. The right call depends on individual financial situations, long-term goals and lifestyle. These decisions deserve serious attention, and the truth is, all the smaller financial habits built along the way are what actually prepare you for the bigger moments.

The key to investing is understanding the power of compound interest. As a young professional, time is on your side. The best starting point is your workplace retirement plan, like a 401(k). Even small, regular contributions can make a big difference over the years. You have to be disciplined and consistent, as these habits will help you build substantial wealth over the long term.

The 401(k) isn't the only workplace benefit worth understanding. Health insurance options, in particular, deserve a close look during open enrollment. For eligible employees, a high-deductible health plan paired with a health savings account (HSA) can be a smart combination. Contributions into an HSA are pre-tax, which means medical spending goes significantly further than it would from a standard post-tax account.

As Ben Franklin famously put it: “In this world nothing can be said to be certain, except death and taxes.” Fair enough. But while taxes are non-negotiable, their impact on your finances isn't fixed. Understanding tax brackets, the advantages of tax deferral and the potential for tax-free growth opens up options that many people leave on the table. Understanding your options pays off — literally — over the course of your career.

Insurance can feel like one of those expenses that's easy to resent, especially when everything is going fine. But that's exactly the point. It exists for the moments when things aren't fine, particularly for low-probability events that could carry major financial consequences. While some coverage, like auto insurance, is legally required, other types, like disability insurance, can be just as critical to maintain long-term financial stability. Whether it's available through an employer or needs to be sourced independently, understanding what's covered (and what's not) is essential.

The 50/30/20 rule is a straightforward budgeting method that assigns every post-tax dollar a specific purpose across three categories: 50% toward needs, 30% toward wants and 20% toward savings or debt repayment. It's approachable, flexible and provides genuine confidence in day-to-day spending while keeping long-term goals in focus. Stacking it with a strategy like no-spend months can accelerate savings momentum even further.

Building a good credit score comes down to consistently demonstrating responsible borrowing over time. Payment history carries the most weight, making on-time payments is non-negotiable. Credit utilization (keeping balances well below credit limits), length of credit history, variety of account types and recent inquiries all contribute to the overall number. There's no shortcut, but steady, responsible habits compound into a strong score over time.

A debit card draws directly from available checking account funds — spending is capped at what's actually there. A credit card allows borrowing up to a set limit, to be repaid later. The tradeoff: Debit cards offer built-in spending discipline but don't help establish a credit history. Credit cards can build credit when used responsibly but carry the risk of interest charges if balances aren't paid in full each month. They're different tools and the best time to understand the difference is before the bill arrives.

Taxes are inevitable but paying more than legally required isn't. Understanding current tax brackets, available deductions and how different investment accounts are taxed makes an enormous difference in long-term financial outcomes. Concepts like tax deferral through a traditional 401(k) or tax-free growth potential within a Roth IRA can significantly multiply wealth over your career. The earlier the planning begins, the better the results.

Minimizing your debt starts with understanding what's owed, to whom and at what interest rate. The most effective strategy typically involves tackling higher-interest obligations first while maintaining minimum payments on the rest, often called the avalanche method. Being proactive rather than reactive with debt not only saves money on interest, it builds financial stability far sooner than a passive approach ever would.

A Health Savings Account offers a triple tax advantage: Contributions are tax-deductible, funds grow tax-free and withdrawals used for qualified medical expenses are completely untaxed. It's a specialized benefit tied to high-deductible health plans and it's one worth taking seriously during open enrollment. For those who qualify, it's one of the most tax-efficient tools available in the entire benefits package.

Compound interest is what makes long-term investing powerful — returns are earned not just on the original investment, but on all the returns already accumulated over time. For young investors, time is the single greatest investing asset. Making consistent, disciplined contributions to retirement accounts early is the standard-setting move for building real long-term wealth.

By getting comfortable with these ten areas of financial literacy, the foundation for a secure financial future becomes a lot more concrete. For personalized guidance through any of these steps, connect with an advisor to turn your knowledge into action.