SUMMARY

Understand what a credit score is, along with how to build and increase your score with our comprehensive guide. Learn about who may review your credit history, safe ways to monitor your score and effective strategies for building credit from scratch.

Navigating the world of credit scores can be daunting but understanding how they work is crucial for financial health. A good credit score can open doors to getting approved for an apartment, favorable interest rates for mortgages, insurance, cars and other loans, while a poor score can close them just as quickly. Here’s a comprehensive guide on how to understand, build and increase your credit score.

What is a credit score?

A credit score is a numerical expression based on a person's credit history, which represents the creditworthiness of an individual. This score is a result of what’s on your credit report. Lenders, such as banks and credit card companies, use credit scores to evaluate the potential risk posed by lending money to consumers. Credit scores typically range between 300 to 850.

Credit scores are calculated through three major credit bureaus – Transunion, Experian and Equifax – which each have their own formula to compute their scores. There’s also a Fair Isaac Corporation (FICO), or a blended credit score, that’s an average of all three. At Johnson Financial Group, we use FICO for mortgage loans and other credit pulls. Remember, credit scores are a snapchat of your current score so while they may be a great reference point, they may not be totally accurate if a lender pulls your score too early or too late in the application process.

What’s a good credit score and why does it matter?

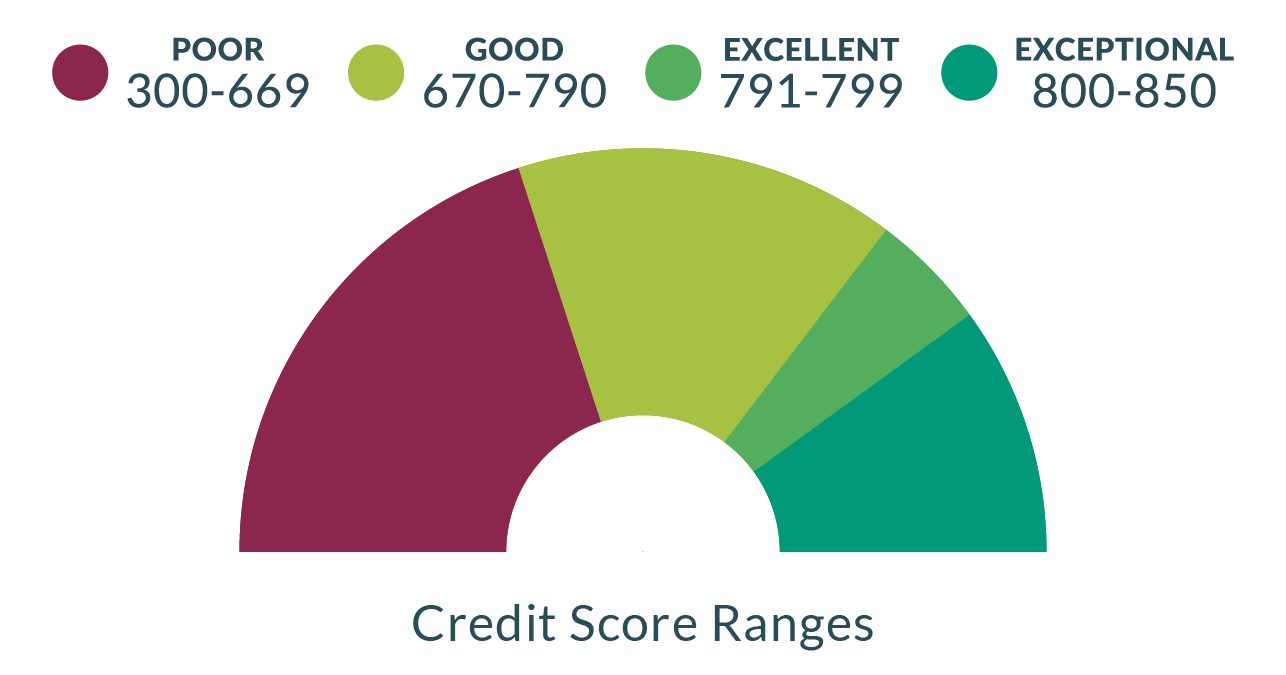

A good credit score typically falls within the range of 670 and above. Anything above 790 is considered excellent, while those above 800 are deemed exceptional. These scores indicate to lenders the individual is a low-risk borrower, which often results in more favorable credit terms.

A good credit score is crucial because it affects your ability to borrow money or access products like credit cards with reasonable interest rates. The closer you are to 850, the more likely you are to be offered lower interest rates on mortgages, car loans and other financial products. A good credit score can influence renting decisions, insurance rates and even employment opportunities, as landlords, insurers and employers may view a good credit score as indicative of responsibility and reliability.

What factors affect your credit score?

Understanding the factors that affect your credit score is crucial for managing your financial health. This section will explore the key elements that influence your score, providing you with the knowledge to make informed decisions about your credit.

- Payment History (35%): This is the most significant factor affecting your credit score. It reflects whether you have paid past credit accounts on time. Missed or late payments can negatively impact your score whereas making payments on time improves your score.

- Amounts Owed (30%): This is measured by your credit utilization ratio, which is the percentage of your credit limit that you're currently using. Aim to keep your credit utilization ratio under 30%. This allows you more financial flexibility while making you more attractive to lenders.

- Length of Credit History (15%): Longer credit histories are favorable because they provide more data on your spending habits and repayment behavior. Instead of closing an older line of credit or credit card, keep it active to show you have a longer history of credit.

- Credit Mix (10%): This refers to the variety of credit products you have, including credit cards, installment loans, finance company accounts and mortgage loans.

- New Credit (10%): Opening several new credit accounts in a short period of time can be seen as risky by lenders and might temporarily lower your score.

What are some safe ways to monitor your score?

Monitoring your credit score is important for managing your financial health. Here are some safe ways to keep an eye on your score:

- Credit Card Companies: Many credit card issuers provide free credit score monitoring to their customers. These are typically updated monthly.

- Credit Monitoring Services: You can subscribe to a credit monitoring service that alerts you to changes in your credit report. Some of these services are free, while others charge a monthly fee. If you have a MyJFG account, you can track your credit score, receive credit reports, educational articles, etc. through My Credit Score and Report.

- Annual Credit Report: You are entitled to a free annual credit report from each of the three major credit reporting agencies — Equifax, Experian, and TransUnion — through AnnualCreditReport.com. This report provides you with an overview of your credit accounts, balances and payment history so you can monitor your credit history but keep in mind that it does not provide a score.

What are a few ways you can increase your credit score?

Building and increasing your credit score is an essential step towards financial stability and unlocking opportunities for major purchases. Here are some practical strategies and habits to help you improve your credit score effectively:

- Pay Your Bills on Time: Since payment history is a significant component of your credit score, paying your bills on time is the most important thing you can do to improve your score.

- Keep Balances Low on Credit Cards: High outstanding debt can affect a credit score. Aim to keep your credit utilization ratio under 30%. The closer you get to your credit limit, the more you may be deemed as a “risky borrower.”

- Avoid Opening Too Many New Accounts at Once: Each time you apply for credit, it can cause a small dip in your credit score. Opening many accounts in a short time frame can compound this effect.

- Check Your Credit Reports Regularly: Errors on your credit report can affect your score. Regularly checking your credit report allows you to correct any inaccuracies.

- Have a Mix of Credit Types: Responsibly managing a mix of credit types, such as a car loan, a credit card and a mortgage, can have a positive impact on your credit score.

How can I build credit if I don’t have any credit history yet?

Starting from scratch with no credit history can be a challenge but it's an important step towards establishing your financial independence. Here are a few effective strategies to begin building your credit when you're starting with a blank slate.

- Get a Credit Card: For individuals without a credit history, securing a credit card may involve applying for secured card(s), that are backed by a cash deposit, or cards specifically designed for beginners, which generally require a deposit or have lower credit limits. It’s important to read the terms carefully and choose a card that reports to the major credit bureaus to effectively start building a credit profile through timely payments and responsible use.

- Set Up a Credit Builder Loan: Credit builder loans are designed to help individuals build or improve their credit scores by allowing them to make regular payments towards a loan, the proceeds of which are released upon loan maturity. These loans are a good starting point for those with minimal or no credit history, as the lender reports the payment activity to the credit bureaus, thereby helping to establish a positive credit record.

- Sign Up for Retail Credit Cards: Signing up for retail credit cards can be a beneficial strategy for those looking to build or improve their credit, as these cards often have more lenient approval criteria compared to standard credit cards. However, it's important to manage these cards wisely by keeping balances low and making payments on time, as high interest rates and the potential for accumulating debt can negate the benefits of building credit. A best practice would be to make a purchase at a retail store and set a reminder to pay the balance at the end of the week or the month before the payment is due.

- Become an Authorized User for a Credit Card: If you have a family member or a spouse who already has credit, you can get added as a joint authorized user on a credit account. This is a strategic way to build credit because it allows you to benefit from the primary cardholder's credit habits, as the account's history will be reported to the credit bureaus under both names.

Understanding and improving your credit score is a vital part of financial literacy. It requires discipline, patience and consistency. By following these guidelines, you can build a strong credit history to pave the way for better financial opportunities. Remember, credit scores don't change overnight but the steps you take today can significantly improve your financial future.

Have more questions? Whether you are looking to build credit or are considering buying a home, connect with a relationship banker or a mortgage loan officer to learn more.

ABOUT THE AUTHOR

AVP Community Mortgage Loan Officer | Johnson Financial Group

With more than a decade of experience in retail banking, Edson joined Johnson Financial Group in 2016 as Community Mortgage Loan Officer. His goal is to help people achieve their goal of homeownership, regardless of their financial situation. He is passionate about working with clients to find the best mortgage product to suit their needs. Because every person’s situation is different, he lets his customers know they are in the “driver’s seat”. Edson believes that success isn’t always measured in numbers. Success means bringing a smile to his clients' faces and making sure they are satisfied with the home buying process.