Some clients enjoy knowing how we make investment strategy decisions. Others have no interest—and, in fact, would rather not know how the sausage gets made (as long as it’s good). This week’s commentary is for the “tell me about it” camp. I thought I would take a minute and explain how the recent decision to increase our small-company stock exposure in client accounts came to fruition.

The “sell” decision

JFG sought to reduce small-company stock exposure in client accounts a little over a year ago because of economic uncertainty. There have been a number of studies around the size of companies and how they react when the economy slows down or when we approach different points in the economic cycle. When the economy slows, all else equal, small-company stocks tend to have a more challenging time and tend to underperform larger companies.

When to buy again?

As with any investment choice, a “sell” decision requires revisiting. When should a “buy” follow?

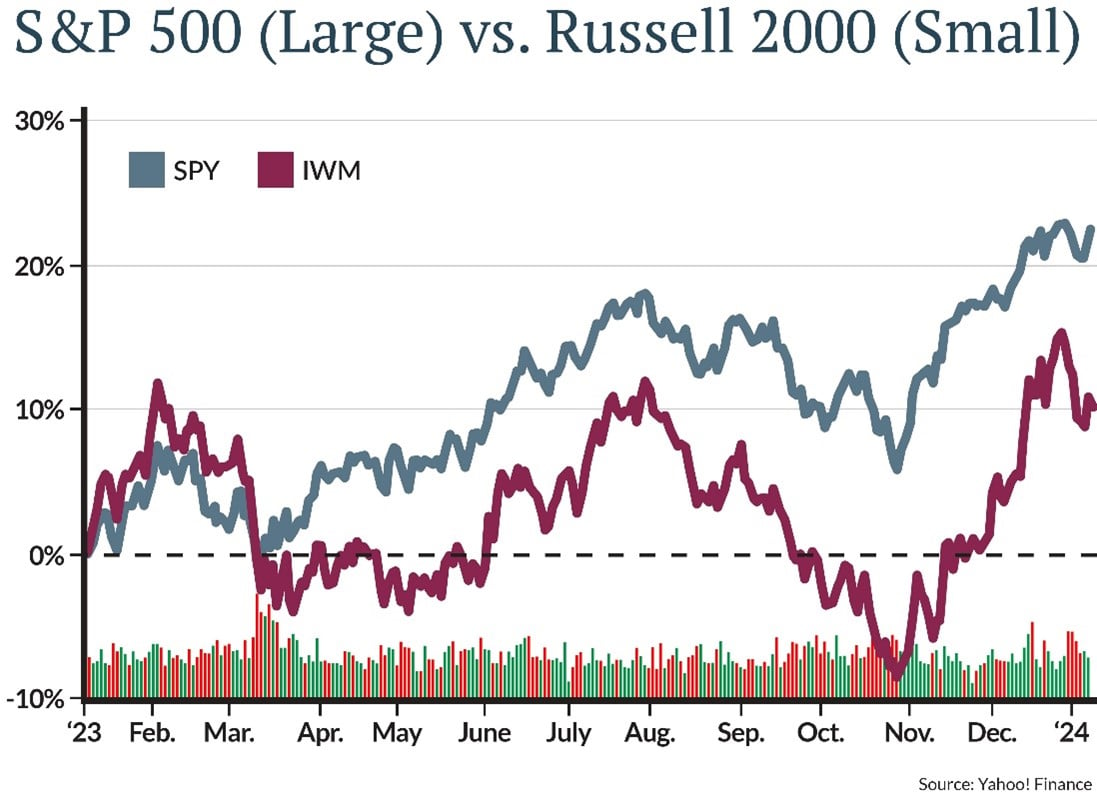

As it turned out, the economy did slow over the last year (though at least at this point, it has not entered a technical recession). The performance of small-company stocks, however, followed the pattern we expected. Over the last year, large-company stocks represented by the S&P 500 Index were up 26.3%, while small companies as represented by the Russell 2000 Index were up 16.9%.

The gap in the chart below shows that difference in returns.

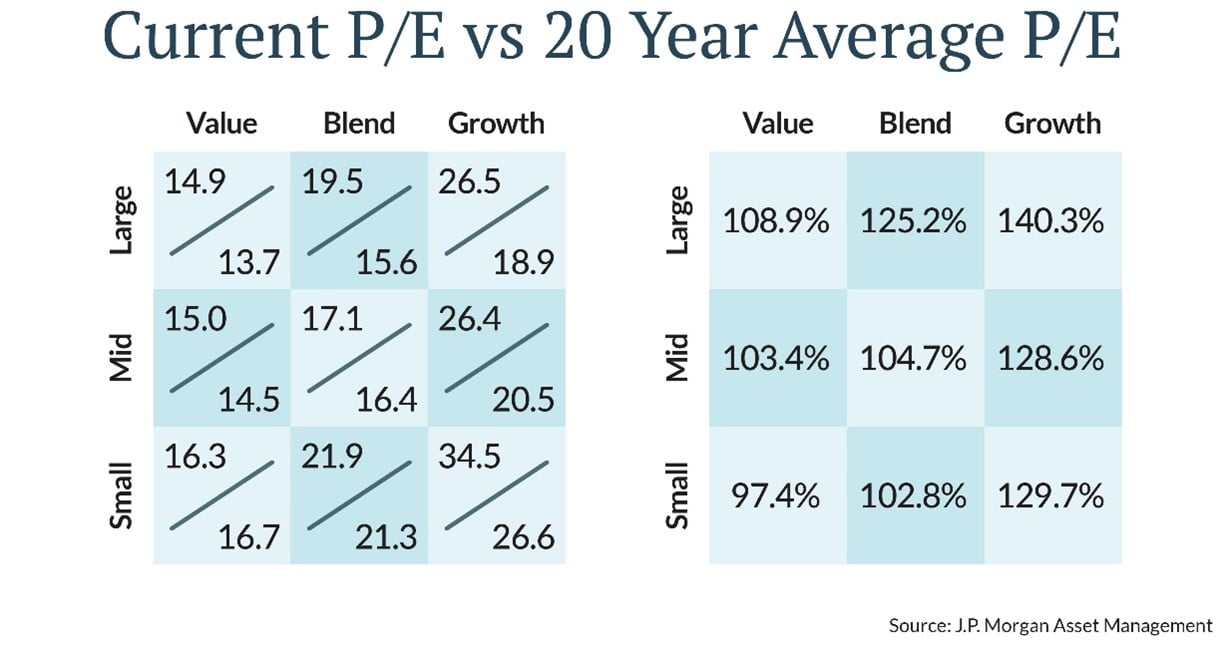

That data point brought us to the next potential decision point. Has the disparity in returns reflected the economic cycle softening we expected? We reviewed a great deal of economic data and valuation metrics to make that decision. For example, the valuation of large- versus small-company stocks also shows small companies to be historically cheaper than large-company stocks based on a price-to-earnings (PE) ratio metric. The smaller the number, the more attractively valued the stock is.

That data point brought us to the next potential decision point. Has the disparity in returns reflected the economic cycle softening we expected? We reviewed a great deal of economic data and valuation metrics to make that decision. For example, the valuation of large- versus small-company stocks also shows small companies to be historically cheaper than large-company stocks based on a price-to-earnings (PE) ratio metric. The smaller the number, the more attractively valued the stock is.

The problem with either return disparities or other valuation metrics is that they are terrible timing tools. These kinds of differences can persist for a prolonged period of time.

The problem with either return disparities or other valuation metrics is that they are terrible timing tools. These kinds of differences can persist for a prolonged period of time.

So, the last part of the decision process is really identifying the catalyst for this environment to change. For this decision, it is our view that the economy has meaningfully slowed from the peak, and the Federal Reserve is likely to be at the end of its tightening cycle.

Although the economy could slow more in the coming quarters, all these data points taken together prompted us to seek an increase in our small company stock exposure to capture the potential rebound in these stocks and the economy as it occurs. Importantly, small-company stock rebounds tend to last for up to three years, so getting the exact bottom, if even possible, is not necessary to capture the performance recovery.

We also intend to continue to review the option to potentially increase our small-company exposure as additional data points become clear. Whether you enjoy knowing how the sausage gets made or not, the choice to increase our small company stock exposure has shown positive results so far.