At This Rate: Financial Institutions Dealing with Higher Interest Rates and Lower Loan Demand

Share

- At This Rate: Financial Institutions Dealing with Higher Interest Rates and Lower Loan Demand

- Here We Go Again: What To Gather Before You File

- These are Wisconsin's Fastest-Growing Banks by Real Estate Lending

- Mortgage Rates on the Decline: Should You Refinance in 2026?

- Meet the RIA: Johnson Financial Group

- Airline Pilots Need a Special Breed of Advisor

- 3 Big Changes to Your Money That Financial Experts Say to Prepare for in 2026

- To Refi Or Not To Refi? Advisors Say It Depends

- Johnson Financial Group's Jim Popp On Staying Local and Investing in Wisconsin Communities

- When the Inheritance is Junk to Heirs, Advisors Need a Plan

- AI: A New Mom’s Best Friend

- 7 Best Investments to Buy in a Recession

- For Financial Advisors, Hosting Holiday Parties Is Out. Here’s What’s In:

- Brother-Sister Duo Paying it Forward in Racine

- Banks Tap AI in Technology Arms Race Against Fraud

- Living Up to Lofty Expectations

- Do I Want Private Market Assets in My 401(k)?

- How ‘One Big Beautiful Bill’ Tax Code Changes Impact Succession Planning

- Corporate Charitable Contributors in Wisconsin

- Johnson Financial Group Investing in Dane County Bank Branches

- Educating Your Board About Optimizing Cash Management

- Alternative Assets in Defined Contribution Plans

- Busting Three Popular Succession Planning Myths

- Answers to Every Early Retiree's Questions This Year, From a Wealth Adviser

- Wisconsin Bankers Association Honors Sam Johnson as Leader in Banking Excellence

- Jeff Pierce Named President of Johnson Wealth

- The Retirement Landscape with Greg King

- Jim Popp Joins Fox Cities Chamber on Local 5 Live in Green Bay

- What Are Money Market ETFs?

- High Mortgage Rates Are Holding My Retirement Hostage: Can I Still Downsize and Retire?

- How Do I Move From Short-Term Savings to Mid-Term Savings for Unclear Goals?

- Volatility Prompts Banks to Hoard Cash and Implement Financial Hedges

- Why Johnson Financial Group is Investing in its Branch Network

- No, The End Is Not Near for Bonds

- Lifetime Gifting Strategy Part I: The Math of Lifetime Giving

- $14bn Gatekeeper Outlines EM Moves, Real Estate Adds

- Do You Need a Local Bank in 2025?

- Mortgage Rates Ease for the First Time in a Month

- THIS Is How You Can Buy a Great Piece of Undeveloped Land, According to Real Estate Pros

- Retirement Reality Check: Four Risks You'll Want to Avoid at All Costs

- Johnson Bank to Replace Kenosha Branch with Updated Building

- A Rise in 'doom spending': Americans buying more to avoid future high costs

- Johnson Financial Group announces leadership change

- Notable Nonprofit Board Leaders: Alvaro Araque

- Johnson Financials' Ceci: The Longer Uncertainty Lasts, the Deeper a Recession Gets

- Johnson Financial Group's West Milwaukee Branch Wins MBJs Real Estate Award for Retail - New Construction

- Here's What Some Local Economists Say About What's Been Going on With the Stock Market

- How will Trump Administration Impact Wisconsin's Economy? Experts Weigh In.

- As Bear Market Looms, Advisors Turn To Trusted Survival Tactics

- 30 People Shaping Milwaukee’s Future: John Chidester

- Three Essential Estate Planning Steps to Protect Your Nest Egg

- Johnson Financial Group Named #1 in Top State Banks in MBJ's Financial Flex

- Johnson Financial Group Continues Support of Marcus Performing Arts Center With Multi-Year Extension

- Fitness and Finance: Parallels in Achieving Goals

- Business Leader of the Year: Karla Krehbiel

- How Will the Trump Administration Impact Wisconsin's Economy? Experts Weigh In

- Finding 'Your Money's Mission': Local Experts Share How to Succeed at Financial Resolutions

- Changing Winds: What’s Likely to Happen to Taxes, Immigration and International Trade Now That the Election is Over

- CIO Dominic Ceci's Gives Investing Insights on Koss Corp. 'Meme Stock' Craze

- Jim Popp Honored Among BizTimes 275 Most Influential Leaders in Wisconsin

- Dividend ETFs Are Taking Off, But Advisors Recommend Caution

- America's Top Financial Advisory Firms 2025

- Are You Doing Your 401(k) Rollover Wrong?

- Johnson Financial Group Honored with Corporate Philanthropy Award by United Way of Kenosha County

- KABA Names Karla Krehbiel: Business Leader of the Year

- Women of Distinction 2024: Johnson Financial Group

- Johnson Financial Group Breaks ground

- Dominic Ceci: Three Preelection Topics for Wisconsin Investors

- 4 Reasons Why Retirees Should Still Be Checking Their Credit Report

- C-Suite Stars: Here are the Milwaukee Business Journal's Top Finance Executives for 2024

- Johnson Financial Economist on the Election and the Economy

- Johnson's Ceci Sees Normalized Earnings Leading to a Sideways Market

- Most Corporate Charitable Contributors in Wisconsin, JFG Ranks #16

- Deloitte Ranks Wisconsin's 75 Largest Privately-Held Companies by Revenue

- Retirees, It’s Time to Give Yourself a Raise. How to Keep the Cash Flowing for Decades.

- Notable Women in Wealth Management: Kelly Mould

- Coolest Thing Made in Wisconsin Contest Now Open

- Life's Financial Milestones; Expert Shares Formula to Navigate Challenges

- What is the Average Retirement Savings for Gen X?

- Johnson Financial Group's CIO, Tim Brown, Nominated for Prestigious ORBIE Award

- Why One 69-year-old Woman Initiated a 'Gray Divorce'

- Johnson Financial Group Expands Wealth Management Team with David Dauchy and Brad Mazola

- Divorce Rates Among Baby Boomers are Soaring, Putting Women’s Financial Security at Risk

- The Latest Tech Trends in Financial Services with Tim Brown, CIO at Johnson Financial Group

- Johnson's Ceci: Hard Landing Potential Rises Until Rates Start Falling

- Peter Speca Joins Johnson Financial Group

- When Retirees Give Away Too Much Money

- $10bn Shop's Top Gatekeeper Gets ‘Interesting’ With Fixed Income

- After ‘Rock Fight’ in 2023, Banks See Businesses Taking Wait-and-See Approach

- What Does Your Spouse Want in Retirement? 6 questions to Ask

- When Retirees Give Away Too Much Money

- Johnson Financial Group: Expands Presence in Madison New West Towne Location

- Johnson Financial Group Shares Tips for Buying a Home in 2024

- Advisors Urge Caution On Penalty-Free IRA, 401(k) Early Withdrawals

- Donations of Nearly $70K Pour in Following Tool Theft from Waukesha Habitat for Humanity

- Dominic Ceci appointed Chief Investment Officer for Johnson Financial Group

- Associated Bank, Johnson Financial partner to provide funding for affordable-housing project in Madison

- Understanding Interest Rates and Unlocking Financial Power

- Ben Pavlik, Top Corporate Counsel Award

- Your Guide to Women’s Wealth Management

- Tim Sheehy appointed to Board of Directors

- WMC, Johnson Financial Group: Announce 2023 Coolest Thing Made in Wisconsin

- Johnson Financial Group ready to serve Lake Country community

- Most Corporate Charitable Contributors in Wisconsin

- Preparing Clients For The Risk Of Cognitive Decline

- Johnson Financial Group expanding with acquisition in Appleton

- How Big A Gamble Is Monte Carlo For Advisors?

- Johnson Financial Group CEO discusses branch strategy with one set to open and another in the works

- Squire to retire after nearly two decades as Johnson Bank regional president

- Bringing a Personal Touch to Digital Banking

- Table of Experts: Reading the tea leaves

- Checking in on Wisconsin banks

- Beyond Lip Service In DEI

- Johnson Financial Group to sell its insurance business to Boston firm

- Johnson Financial Group plans new branches, including in West Milwaukee

- New Johnson Financial Group Branch Planned In West Milwaukee and Delafield

- Johnson Wealth Fixed Income Tilts at Emerging Markets Debt, Mortgage Backed Securities

- Your Financial Foundation with Al Araque on the Lifeblood Podcast

- Unexpected health insurance surprise possible when pandemic insurance programs expire

- Bond Investors: Be a Prudent Pig, not a Yield Hog

- Women Insurance Pros on Balance, Community and the Future

- Financial Planning For Couples Who Totally Disagree

- How To Help Clients Who Own Businesses in Declining Industries

- Johnson Financial Group presents 'Lightfield' coming to Cathedral Square Park

- Three Essential Estate Planning Steps to Protect Your Nest Egg

- Johnson Financial Group Named Top LGBTQ Workplace

- Financial advice is the midlife job that women want – but don’t know exists

- Expert Insight for Beginner Rental Property Investors

- Coolest thing made in Wisconsin announced by WMC and Johnson Financial Group

- Corporate Charitable Contributors in Wisconsin

- 'Coolest Thing Made in Wis.' voting begins

- Johnson Financial Group and Habitat for Humanity Kenosha work together to help homeowners

- We have a responsibility to be solution providers for our customers

- Being a leader is a team sport

- Jason Herried Joins Chuck Jaffe on Money Life

- Have questions about "Gray Divorce"? Attorney Kelly Mould, CRP® can help.

- Jazz in the Park Is Back Thursday Nights Starting July 21

- People in Business - Al Araque

- 2022 Housing Market Overview: Everything You Need to Know

- "Give Back More Than You Take" - Helen Johnson-Leipold

- A Brief History of Economic Crises, Crashes and Recoveries

- Kelly Mould and Kate Trudell Earn State Bar Award for Outstanding Service

- JFG Supports Affordable Housing through FHLBank Chicago

- Helen Johnson-Leipold shares business tips for success at Marquette speaker series

- Notable Commercial Banking Leaders: Thomas Moore

- Notable Commercial Banking Leaders: Viktor Gottlieb

- Johnson Financial Group partners with Racine Habitat for Humanity to service mortgages at no cost

- Upcoming Lineup Of Broadway Shows Announced At Marcus Performing Arts Center

- See the Milwaukee Business Journal's 2022 Real Estate Award winners

- Joe Maier “Employers are going to have to rethink their practices”

- Emotional Investments: Why They Happen and How to Avoid Them

- Inflation advice for younger colleagues

- Amber Krogman: 40 Under 40

- Evoking change within the Milwaukee community with Johnson Financial Group's Jim Popp

- A Shift in the Tech Landscape

- Evoking change within the Milwaukee community with Jim Popp, CEO of Johnson Financial Group

- The Rising Trend Of "Gray Divorce" with Kelly Mould of Johnson Financial Group

- Evoking change within the Milwaukee community with Jim Popp, CEO of Johnson Financial Group

- Johnson Financial Group Recognized on Financial Planning's 2021 RIA Leaders List

- Find out why these business leaders are 2021 Milwaukee-area power brokers

- Thoughts for business executives on future-proofing a business

- Jim Popp Joins Fox 6 to Announce the Milwaukee Holiday Light Festival

- Milwaukee’s Holiday Lights Festival Kicks Off This Week!

- #FreeBritney: When Protections Turn Toxic

- WisBusiness: the Podcast with Jim Popp, president and CEO of Johnson Financial Group

- WE Energies Customer Spotlight On Energy Efficiency

- Johnson Financial Group donates $500,000 to United Way organizations across Wisconsin

- Madison’s Moving Business Forward Podcast

- Thoughts for business executives on return-to-office technology

- First look: Johnson Financial Group's new Downtown offices and branch

- Johnson Financial Group Shows Off High-Rise Office

- Six Tips for Developing a Business Plan for Uncertain Financial Times

- Is Bitcoin Here to Stay? An Assessment of Opportunities and Risk

- You may have a ‘huge edge over high-powered investors,’ says investing risk expert: Here’s why

- Executive Insights with Jim Popp

- CEO Jim Popp Honored as Distinguished Executive

- Webinar: Cybersecurity Made Simple

- 2021 Guide to Wealth Management: A War on Wealth?

- Notable Alumni: Scott Cooney

- Jason Herried Joins Chuck Jaffe on Money Life Market Call

- Top Workplaces 2021: Q&A with three CEOs who were recognized for their leadership during a challenging year

- How will Biden's new tax plan affect you?

- American Jobs Plan: Potential Implications for You and Your Business

- Get on the Right Track to Financial Freedom

- Greater Madison area Top Workplaces 2021

- The Crazy Housing Market: Buy, Sell or stay on the sidelines?

- UPAF Ride for the Arts series will take place over three June weekends

- Financial services industry helped guide businesses through sharp downturn: Banks hustled to meet massive PPP demand

- Financial services industry helped guide businesses through sharp downturn: Banks hustled to meet massive PPP demand

- Johnson Financial Group matches food donations to help feed Wisconsin families

- Johnson Financial Group: To donate $300,000 to help feed Wisconsin families

- Women in Leadership: Sharing & Celebrating Women's Stories

- 2020 Milwaukee-area power brokers

- Dow Surges to Highest Level Since February on Vaccine Results, Biden Win

- Johnson Financial Group Named One of Wisconsin's Largest Corporate Charitable Contributors

- Don't forget about the "I" in D&I

- Johnson Financial Group to move Milwaukee offices to Cathedral Place

- Pandemic Uncertainty Leaves Wisconsin Bankers Ready To Reserve

- What's going on in the financial markets right now with Jim Popp of Johnson Financial Group

- Downside risk is now a pit, not a chasm. Still, underweight stocks & overweight (some) bonds.

- Why You Want To Keep Your Politics Separate From Your Investing

- Johnson Financial Group growing, still hiring on its 50th anniversary year

- The COVID Calculation

- Pleasant Prairie company gets boost from Paycheck Protection Program

- Banks locally, statewide step up to help businesses obtain $8.3 billion in PPP

- Johnson Financial Group donates $200K to support United Way, other nonprofits during COVID-19 pandemic

- Second round of PPP starts slowly as Milwaukee-area businesses still await loans

- Wisconsin lenders ready to shell out hundreds of millions in Paycheck Protection Program loans

- Planning opportunities under the CARES Act

- BizTimes Media Announces Milwaukee’s Notable Women in Commercial Banking

- Johnson Financial Group adviser honored

- Tech-driven R&D goes beyond the budget. Some Milwaukee execs speak up

- What would cause markets to react after Fed meeting

- Banking official remains confident in local economy's growth

- Rock County home prices continue to climb

- The coolest thing made in Wisconsin

- Dan Defnet named president of Johnson Bank

- Future Returns: Ignore Politics When Investing

- Local banker to get Forward Janesville's Lifetime Achievement Award

- Wisconsin Could See Economic Slowdown This Year, Not Recession

- When Corporate Bonds Are a Risky Investment

- Johnson Financial Group becomes Broadway at the Marcus Center title sponsor

- Getting Ready to Exit: What Baby Boomers know and should know about getting their business ready for sale

- Take Five: Putting some Popp in banking

- Jim Popp in the News

- Jason Herried's Take on the 'Booms and Busts' of the Economy

- Johnson Insurance creates new 'workplace of choice'

- Paul Ryan lauds Harvard award-winner Helen Johnson-Leipold

- Business Leader of the Year Helen Johnson-Leipold leads big parts of the Johnson family business

- Johnson Financial Investment Expert: More growth, low inflation ahead

- Foxconn's Balance Sheet Tipped in Mt. Pleasant's Favor

- JFG honored by Department of Defense

- The Open Road comes to the Milwaukee Art Museum

- 3 business lessons from the new Johnson Financial Group CEO

- Executive Q&A: Jim Popp takes the helm at Johnson Financial Group

- Banking exec Jim Popp named president of Johnson Bank

- Banker: Focus on millennials, not president

- American Birkebeiner Legacy Lives on with Support from Johnson Bank and Johnson Family Foundation

- TEMPO MILWAUKEE 2020

The economy is marked by a “tale of two banking systems,” says analyst Christopher Wolfe.

The managing director of banks for North America at Fitch Ratings, Wolfe said 2023 has been a different experience for institutions such as JPMorgan Chase Bank and Bank of America, which have been relatively unaffected by recent industry turmoil. Chase Bank, for instance, grew as a result of the collapse of First Republic Bank, because it acquired a majority of the failed bank’s assets and some of its liabilities.

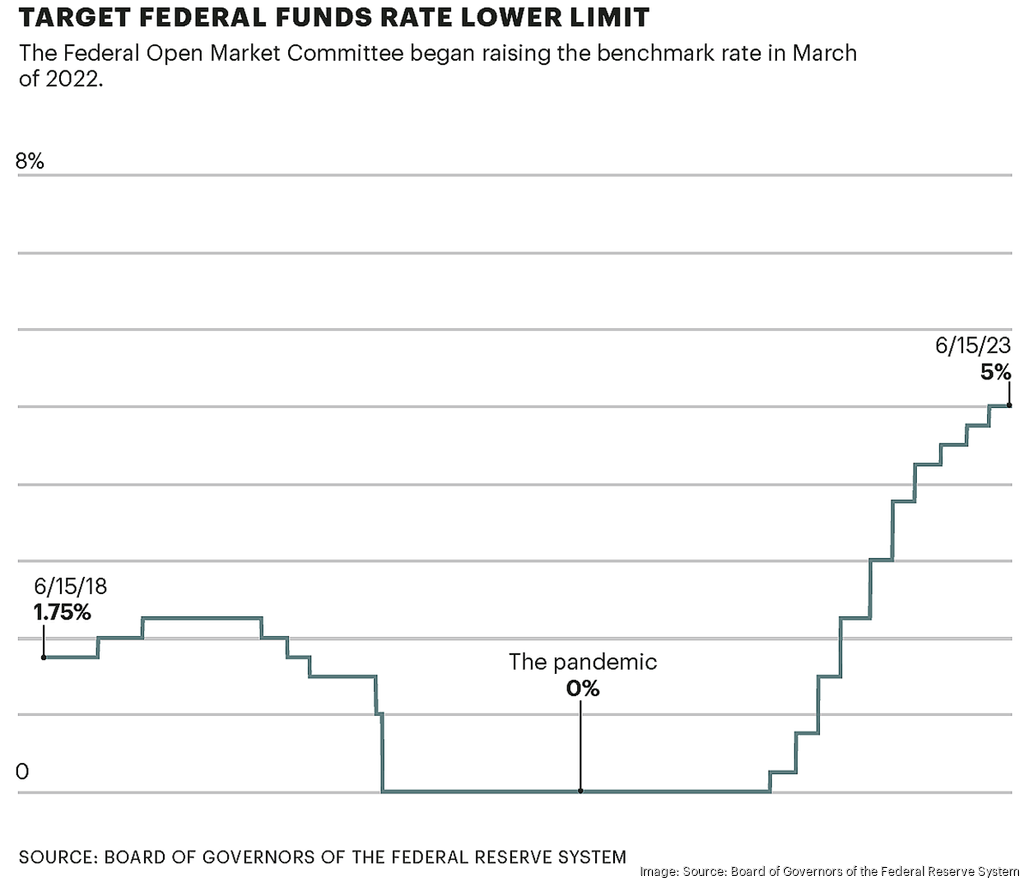

For regional banks, this environment has been another story. Much of the upheaval has settled down, Wolfe said, and the industry appears to be returning to a path of normalizing. In light of the Federal Reserve’s efforts to slow down inflation, Wolfe said liquidity is less abundant, and the credit environment is likely to be tighter than it had been. That creates pressure on banks’ bottom lines, he said.

Banks nationally had net income of $79.8 billion in the first quarter of the year, according to the Federal Deposit Insurance Corp. That was up about 16.9% from the fourth quarter of 2022, when the acquisitions of two failed banks are included. Excluding those purchases, the FDIC said, net income would have been flat from the prior quarter.

Looking ahead, Wolfe said he anticipates loan growth will be softer this year than last. That could affect everyone from potential home buyers and sellers to business owners and developers.

“I think you’re going to probably see pockets of weakness on the demand side and the supply side,” Wolfe said, highlighting in particular the office segment of commercial real estate.

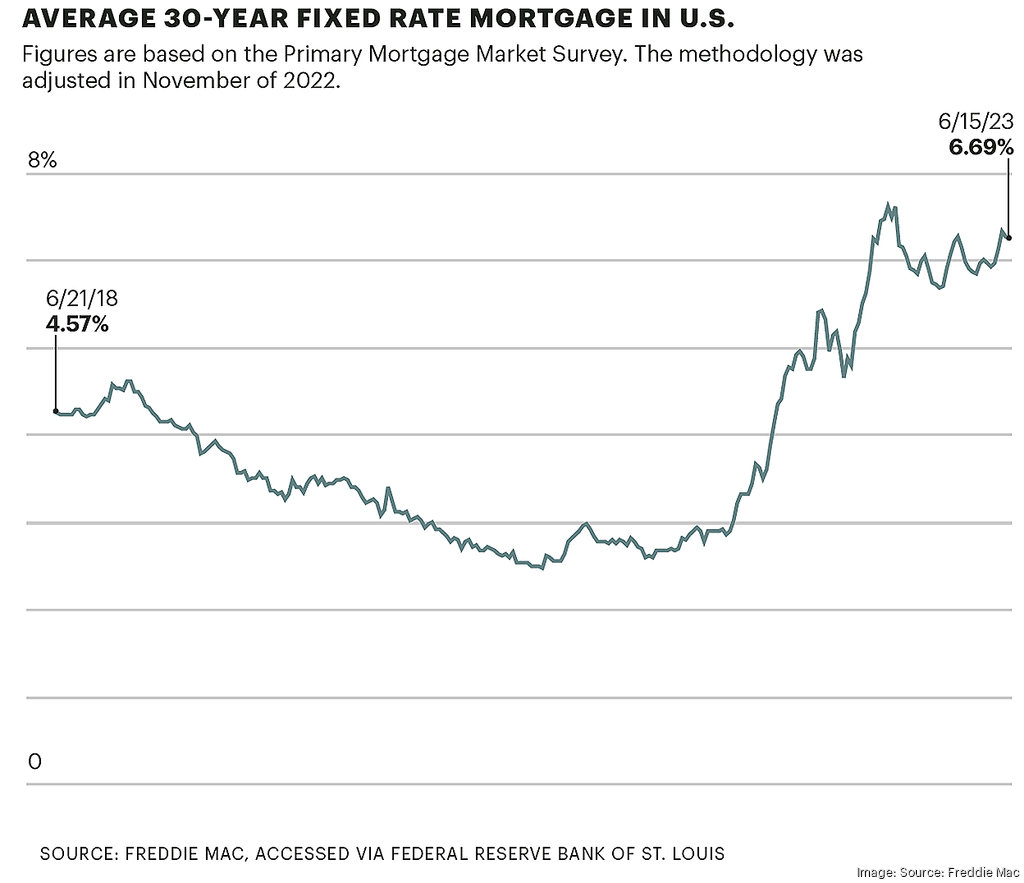

The residential mortgage business is another that has been hurting across the country, driven not only by increasing interest rates but also because of dynamics specific to the housing market. As the Greater Milwaukee Association of Realtors has highlighted, construction of single-family houses and condominiums has slowed, and demand for a home to purchase outstrips the available supply.

Meanwhile, bank executives told the Milwaukee Business Journal, people who locked into a lower interest rate are reluctant to sell their homes and take on debt at a higher cost.

Research by the Mortgage Bankers Association found the average production volume per company fell from 16,590 loans and $4.9 billion in 2021 to 8,371 loans and $2.6 billion last year at independent mortgage banks and the mortgage subsidiaries of chartered banks.

The downturn in the mortgage market has resulted in lenders locally and nationally revising their operations. Pewaukee-based Inlanta Mortgage Inc. for instance, sold to a San Diego firm called Guild Mortgage, citing the dampened demand for mortgages.

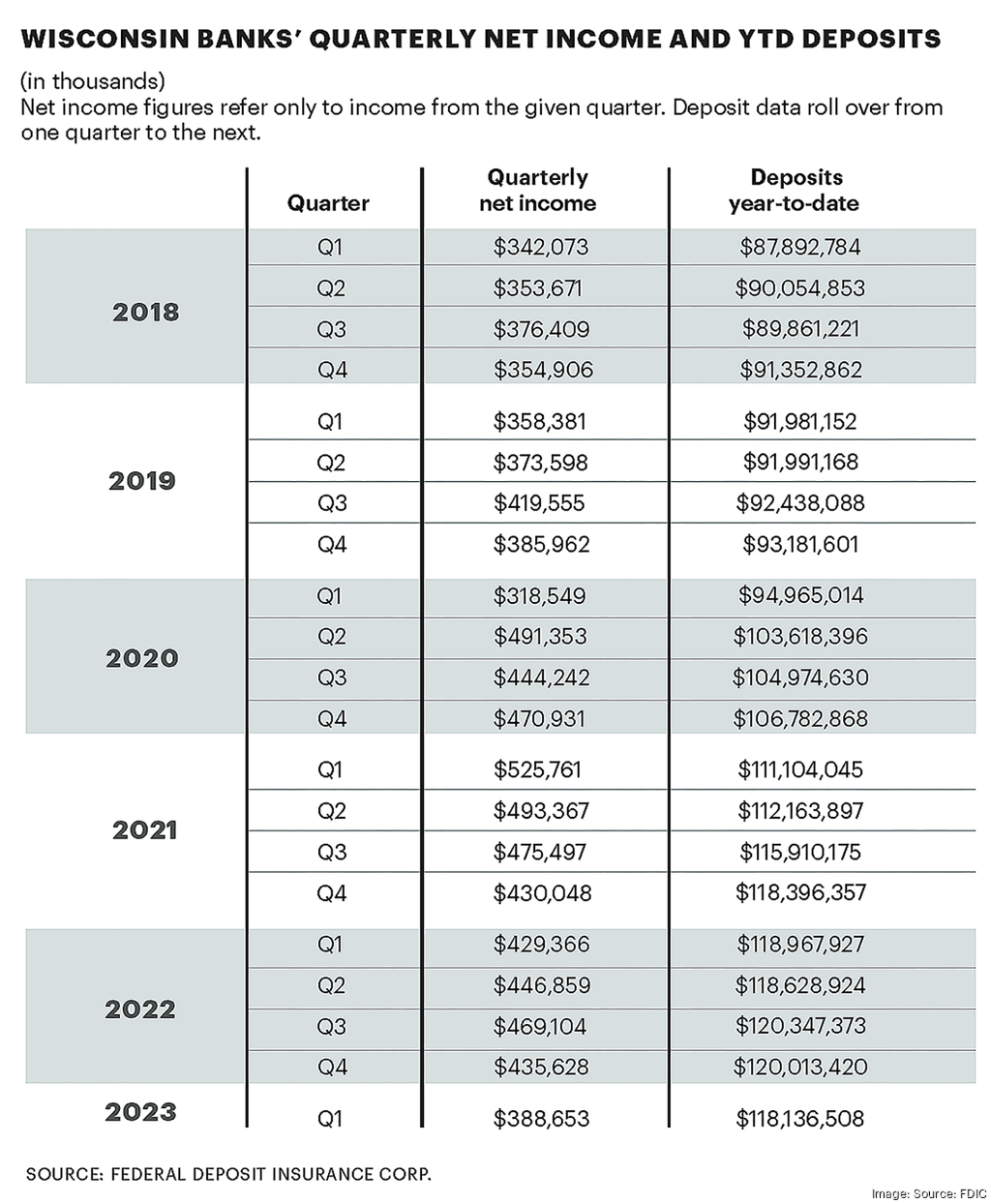

More recently, Colonial Savings in Fort Worth, Texas, announced in mid-June it would stop originating mortgages. Bank net income depositsexpand Bank net income and deposits

David George, a senior research analyst at Baird who covers U.S. banks, said financial institutions also are in a “food fight” for deposits, and originating new loans is less attractive.

Relative to the past couple years, which George said were characterized by “healthy growth,” loan growth rates are reverting to a more typical level.

“(Banks are) focused on managing the economics of their balance sheet,” George said. “You’re seeing some banks start to de-emphasize lower yielding loans that don’t make economic sense or pricing themselves out of markets that may not meet their return profile or characteristics or risk and reward characteristics.”

The Milwaukee Business Journal spoke with executives from local banks about how they’re navigating this environment. Read on for their perspectives.

Johnson Financial Group

The credit crunch is real, says Johnson Financial Group CEO Jim Popp, and that makes credit more valuable.

Popp, whose organization owns Johnson Financial Group, said the credit crunch is a function of the Federal Reserve trying to cool the economy and slow inflation. Now, all financial institutions are determining the best uses of their balance sheets under the circumstances, “because we only have so much of it,” Popp said.

The environment has shifted from earlier in the pandemic, when he said deposits were not worth as much and loans were cheap. Now, Popp said, banks’ cost of capital has increased, and financial institutions are paying depositors higher rates as a “fight in the streets right now for deposits” wages on.

From a mortgage perspective, Popp said the pipeline of approvals is strong, but transactions are down. That’s not because people can’t obtain credit, he said, but because they’re unable to find a house to purchase.

On the commercial side, he said some Johnson Financial Group borrowers are taking out less than they might have otherwise, because of the increased cost of capital and uncertainty in the market. That means customers are deciding whether to go ahead and construct a new building or acquire equipment.

On the other hand, Popp said, customers who have hit their borrowing limits at other institutions are turning to Johnson Financial Group.

“All of a sudden, business is calling us, and you’re getting inbound calls from individuals and companies who want to borrow money, because they’re feeling the crunch where they are today,” Popp said.

By the Numbers

Johnson Financial Group: (Metrics as of the end of 2022)

Assets: $6.1 billion

Net loans and leases: $4.4 billion

Net income attributable to bank: $57.4 million

Net interest margin: 3.27%